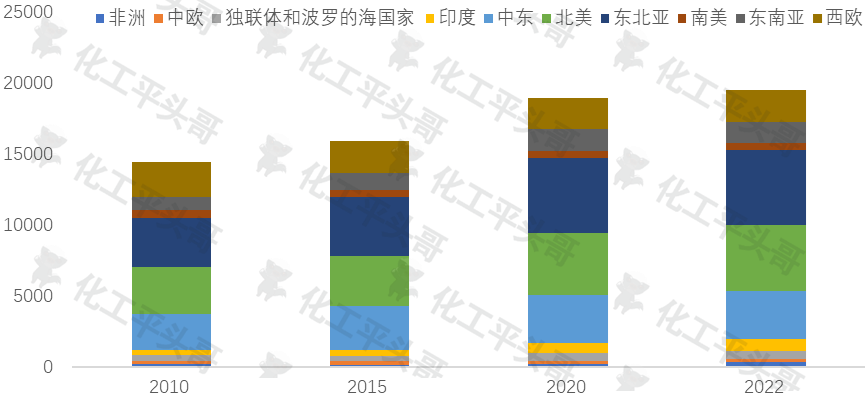

From the changes of global ethylene production capacity in the past 10 years, the following characteristics can be summarized: First, the production capacity in North America, Northeast Asia and the Middle East has a fast growth rate, especially the developing countries represented by China, which has driven the rapid development of production capacity in Northeast Asia. Second, naphtha cracking was the main production method until 2020, but in recent years, light hydrocarbon cracking has become a new growth point of ethylene production, mainly due to the shale gas revolution in the United States, which led to the explosive growth of global ethane supply, providing a continuous supply of raw materials for ethylene production.

North America has been the world's leading ethylene producer. Due to competitiveness, North America's ethylene utilisation rate fell below 80% in 2008, with 2.4 million tonnes of capacity lost between 2008 and 2010. After 2011 years as the U.S. shale gas revolution raw material supply of cheap ethane explosive growth, promote ethylene capacity 迚 again into the expansion cycle of North America.

Between 2015 and 2020, the U.S. Gulf Coast added 13 mmTpy of ethylene capacity, bringing the total U.S. ethylene production capacity to over 40 mmtpy, making it the world's largest ethylene producer. After 2020, all of the new ethylene production capacity in the United States will be produced by cracking light hydrocarbons, of which 82% will come from ethane as a by-product of shale gas and 18% from propane and butane as a by-product of shale gas. It can be said that the shale gas revolution in the United States has achieved the comprehensive competitiveness of the American ethylene industry.

Figure 2 US ethane Production over the years (Data source: EIA)

For China, the growth of its ethylene capacity is the main driving force for the overall capacity growth in Northeast Asia. 迚 into the 21st century, China's ethylene capacity have two rounds of focus on the period: 2005-2006 and 2009-2010, is mainly due to the growth in domestic demand, the three barrels of oil refinery 迚 increases production line. In ten years from 1999 to 2008, ethylene production capacity of 4.35 million tons grew to 9.985 million tons per year. By the end of 2009, the national ethylene production capacity broke through ten million tons for the first time, reaching 11.778 million tons per year, ranking the second place in the world.

Since 2011, due to the continued high oil price and the loss of discourse power over crude oil, China has increasingly considered energy security. Since 2011, there have been a lot of ethylene production using coal and methanol as raw materials in China, opening a chapter for the diversification of ethylene production and supply in China.

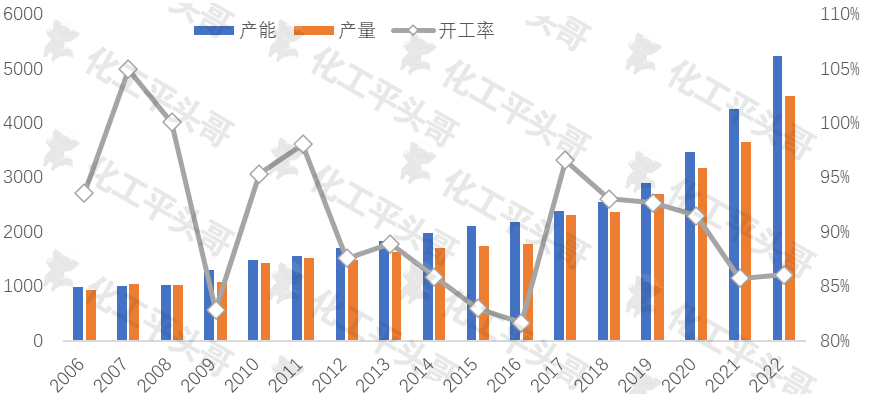

Figure 3 Changes of ethylene production capacity in China over the years (Unit: 10,000 tons)

For the future, will China stay ahead of the US as the world's largest ethylene producer?

First, China's 2030 carbon peak requirement is a major barrier to the scale of its chemical industry. Before the carbon peak, the scale of China's chemical industry will take the lead to reach the peak, in order to prepare for the overall peak, and ethylene as a key product of basic chemical production, and the scale of investment is huge, will also be the main method to control the chemical industry to reach the peak. Therefore, the growth of China's ethylene industry in the future may be affected by the approaching peak date, and gradually urban growth momentum.

Second, US ethylene additions continue to slow. Since the end of 2014, as a result of which 栺 fell sharply, together with the disease caused by falling demand, north American petrochemical investment expansion pace in recent years show obvious signs of slowing.

Thailand's PTT Global Chemicals (PTTGC) has once again postponed its ethylene project in Belmont, Ohio, with the future of the project uncertain as South Korea's Daelim has withdrawn from the project in 2020, according to Donghai Securities. In October 2020, Chevron Phillips Chemicals postponed a final investment decision on its 2 mmTpy ethylene and high-density polyethylene (HDPE) joint venture cracking project with Qatar Petroleum on the U.S. Gulf Coast. Front-end engineering for the project has been completed. Formosa Petrochemical (FPCC), a unit of Formosa Plastics Group, plans to start production of two 1.2 million tonne ethane cracking units in Louisiana in 2023. In October 2019, the company was fined $50 million for pollution and ordered to make improvements to zero plastic emissions. The company later said it would delay construction of the project.

According to incomplete data statistics, the proposed scale of ethylene projects under construction in the United States in the future is about 5.11 million tons/year. If the project is fully operational, U.S. ethylene production will reach 49.93 million tons per year in the next five years.

As a result, China will remain the world's largest ethylene producer in the next five years, assuming that both Chinese and American ethylene projects come on stream as scheduled, and the gap between the US and China will widen.

Finally, ethylene is the basic and key product of the chemical industry. The slowing down of ethylene industry will also be the main reason for the slowing down of chemical industry. In the future, China will continue to expand the capacity of ethylene industry, which also represents that the scale of China's chemical industry will continue to expand in the future.