Rongbei Technology (688005.SH) and Dangsheng Technology (300073.SZ) are the oldest "double leaders" in the field of positive electrode materials.

The two leading companies actually have some origins: Bai Houshan, the controller and chairman of Rongbai Technology, was the legal person, director and general manager of Dangsheng Technology from December 2001 to March 2012. Under his leadership, Dangsheng Technology rapidly grew into a global leading supplier of lithium cathode materials. By 2010, Dangsheng Technology's market share had reached the second in the world and the first in China. Became a veritable industry leader at that time.

However, with the change and impact of industrial competition and technological trends, great changes have taken place in the field of cathode materials. Time back to 2021 and before, there is no company in the world of positive electrode materials sales revenue exceeded 10 billion yuan mark, at that time, Rongbai Technology and Dang Sheng Technology with 9.575 billion yuan and 7.876 billion yuan (positive electrode material revenue) ranked first and second in the industry, and said that positive electrode materials "double leaders".

However, only one year later (2022), there are 11 companies in the A-share listed companies "positive electrode materials" annual sales exceeded 10 billion yuan, of which the strong rise of Hunan Yuleng with 614.98% of the ultra-high growth rate, jumped to become the top 1 manufacturers in the field of positive electrode materials, Wang hundred technology fell to second, when rising technology has fallen to fifth.

Entering 2023, under the influence of the fierce expansion of the industry, the big reshuffle and price war are fierce.

First of all, according to research institute EVTank data show that in 2023, China's lithium ion battery cathode material shipments of 2.476 million tons, an increase of 27.2%, far lower than the growth rate of 77.97% in 2022. According to 24 tide Industry Research Institute (TTIR) previous statistics, the entire power and energy storage battery core industry chain price plummeted in 2023, of which the power battery fell by more than 44%, the square energy storage battery (lithium iron phosphate) fell by more than 54%, the electrolyte fell by more than 58%, and the price of some positive electrode materials fell by more than 70%. Battery grade lithium carbonate prices fell more than 80%.

In such an industrial situation, even strong business operations such as Rongbai Technology and Dangsheng technology have also suffered significant impact, or even impact.

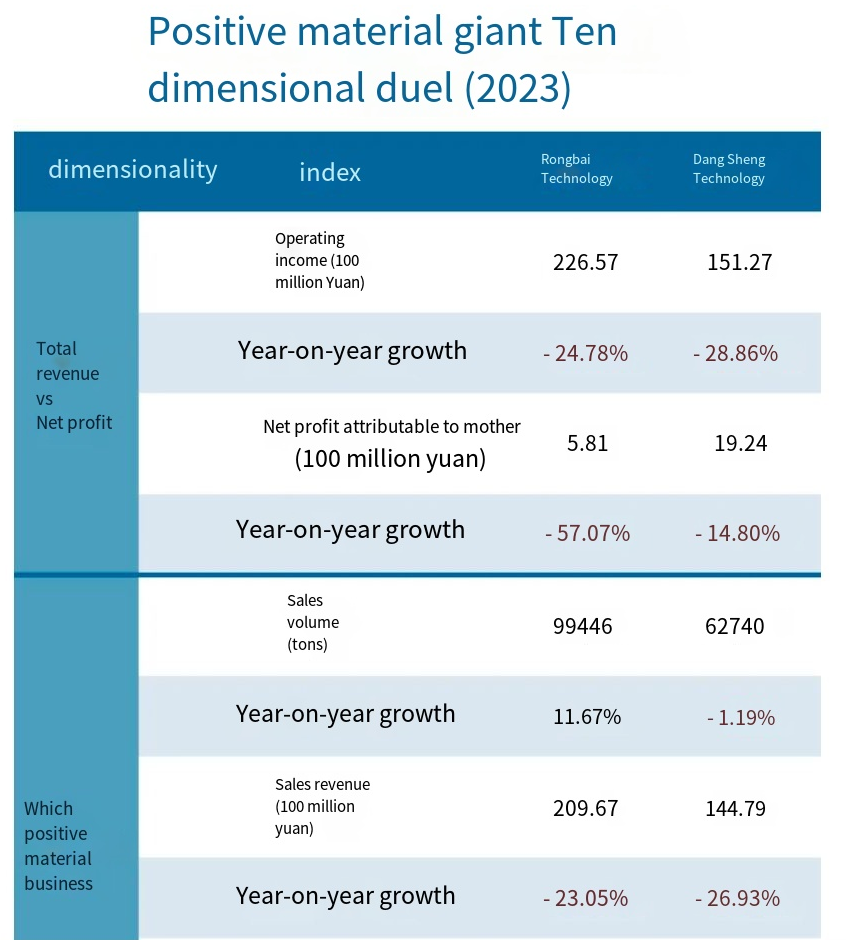

According to the 2023 financial report disclosed by the two, the operating income of Rongbai Technology and Dangsheng Technology fell by 24.78% and 28.86% respectively, and the net profit of the mother fell by 57.07% and 14.80% respectively.

From the perspective of quarterly trend changes, the industry situation is more severe. For example, the operating income of Rong Bai Technology has declined for three consecutive quarters (the second quarter of 2023 to the fourth quarter), in the fourth quarter, its revenue fell by 62.34% year-on-year, almost the largest decline on record, and even lost 35 million yuan in the fourth quarter (down 108.04% year-on-year), which is its first loss in nearly 16 quarters; When the technology trend is nearly the same, the fourth quarter of 2023 is also near the largest quarterly decline on record (64% year-on-year).

The author also found that in 2023, the capacity utilization rate of the anode material business of Dang Sheng technology was 70.94%, down 62.16 percentage points from 2022.

The more critical the moment, the more test enterprises comprehensive competitiveness and historical background. At present, in the positive material giant Rong hundred technology and Tang Sheng Technology is the first to disclose the 2023 financial report, 24 tide industry Research Institute (TTIR) respectively from the market value, income generation, internationalization, profit, research and development, capital, debt, hematopoitic, staff and efficiency, operating capacity and other ten dimensions of the data comparison, enterprise competitive strength and pressure at a glance.

For example, in terms of revenue generation, Rongbei Technology has far exceeded Dangsheng Technology, and the former's revenue scale is 50% higher than the latter in 2023, but the profit scale (net profit to the mother) is only 30.20% of Dangsheng Technology.

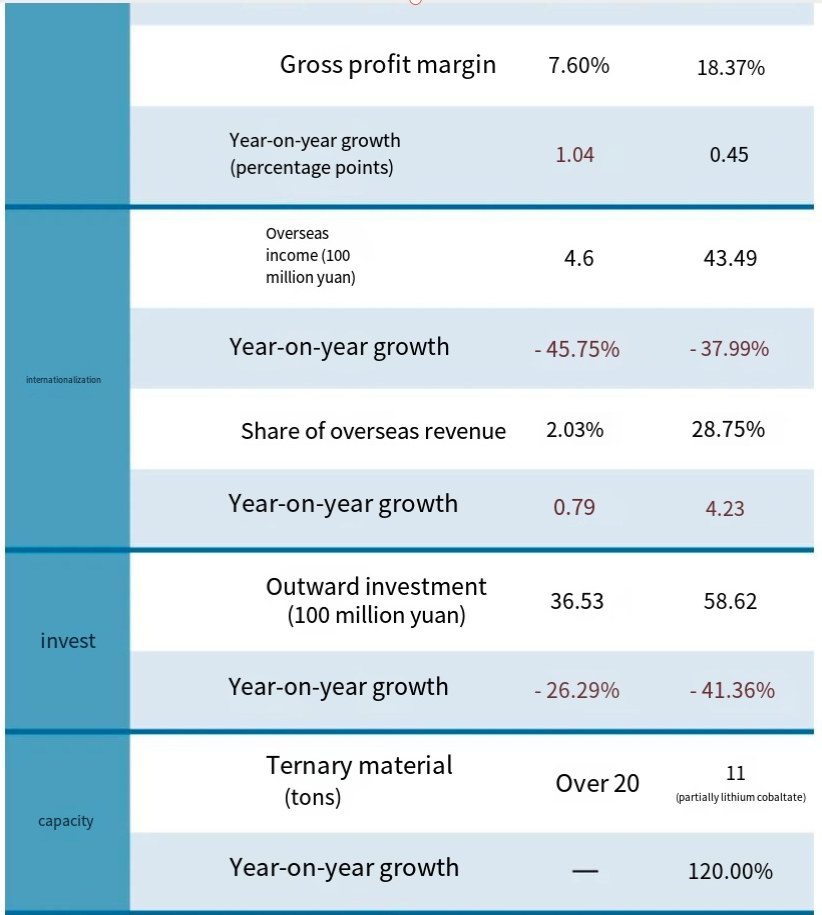

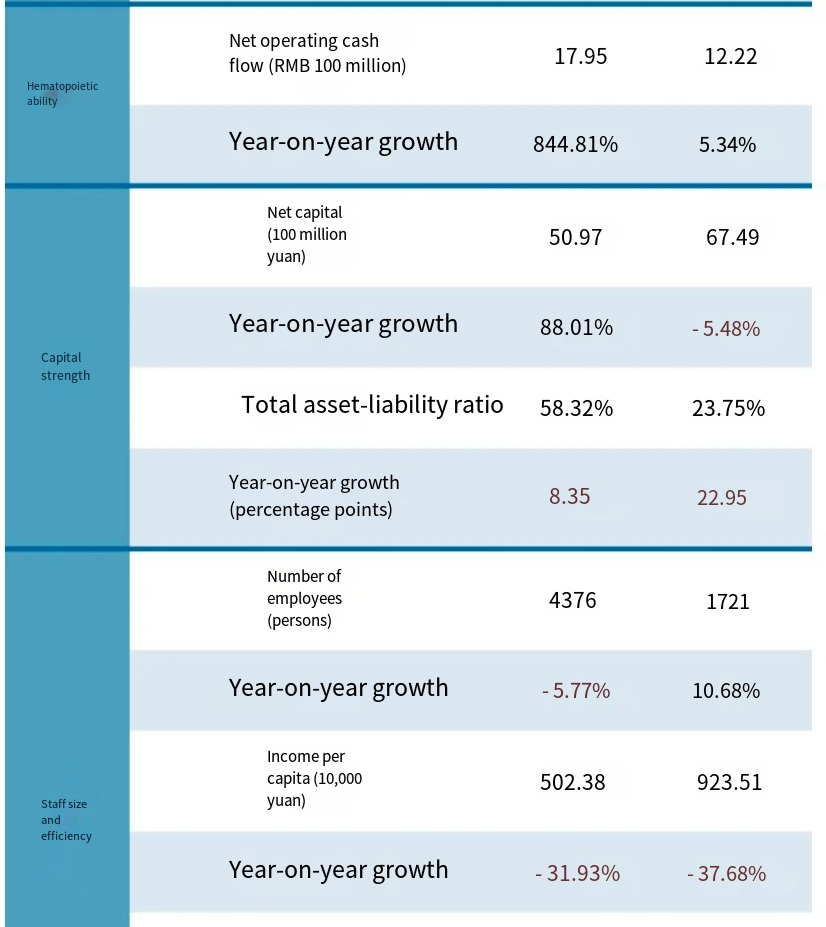

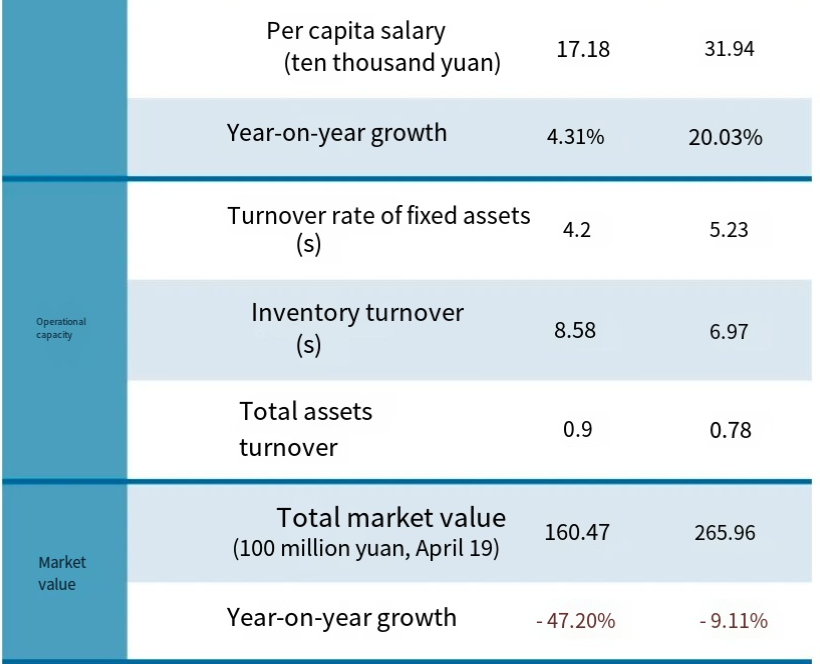

In terms of internationalization, in 2023, the overseas income of Rongbai Technology is about 460 million yuan, while Dangsheng Technology reaches 4.349 billion yuan; In terms of employees and efficiency, Dangsheng Technology has a clear advantage, and its per capita income of employees in 2023 is about 9,235,100 yuan/year, and the per capita salary is 319,400 yuan/year, which is 83.83% and 85.91% higher than Rongbai Technology respectively.

Different core data dimensions often show the strategic advantages, potential risks and pressures at different levels of the enterprise. For the comprehensive strength of the enterprise, I believe readers have their own judgment, we will not go into details one by one, please see the table below.

According to the analysis and prediction of Xinyue Lithium Battery, Soochow Securities and other institutions, the demand for terpolymer cathode materials in 2025 will be about 1.3 million tons, while the supply may reach 1.97 million tons, and the excess capacity will reach 697,000 tons. In 2025, the demand for lithium iron phosphate anode materials is about 2.474 million tons, while the supply may reach 3.612 million tons, and the excess capacity is about 1.138 million tons, both of which show a surplus trend.

According to 24 tide Industry Research Institute (TTIR) incomplete statistics, at present, the total production capacity planning of positive electrode material/lithium iron phosphate announced by 29 domestic enterprises has reached 10.6415 million tons, the capacity planning of overseas enterprises is nearly 1.1 million tons, and the total capacity planning of domestic and overseas enterprises is nearly 12 million tons.

It is almost foreseeable that the positive material circuit will inevitably appear a round of bloody industrial reshuffle, and the low-end production capacity may be cleared in large numbers in the future.