Ethylene is the basic raw material of petrochemical industry, the main downstream derivatives are polyethylene, ethylene glycol, ethylene oxide, styrene, polyvinyl chloride, ethylene-vinyl acetate copolymer and other chemical products.

There are many ethylene production routes in China, and the main industrial routes include naphtha cracking, methanol/coal to olefin (MTO/CTO), olefin catalytic cracking, catalytic cracking/cracking (DCC/CPP), heavy oil efficient catalytic cracking (RTC), ethanol dehydration, etc.

In 2023, the mismatch pattern of domestic supply and demand has inhibited the overall profit situation of the ethylene industry, the limited recovery of demand has inhibited product prices, and the various routes have continued to lose money.

In 2024, the market is expected to be good downstream demand for ethylene, the oil price correction will further benefit the profit performance of the industrial chain, and the industrial chain is expected to achieve break-even, but the situation of excess products and equipment losses will still exist for a long time, and the "big ethylene" era represented by scale competition in the early stage will fully enter the era of cost competition in the next 10 years.

Ethylene routes continue to lose money

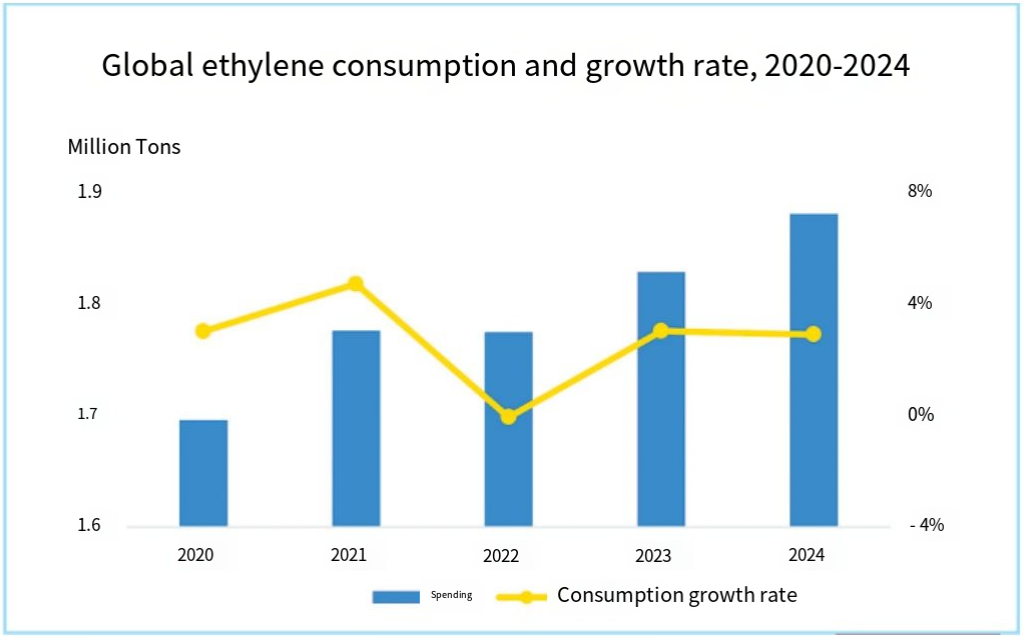

In 2023, the global ethylene capacity increase exceeded 8.7 million tons/year, and the total production capacity reached 228 million tons/year. More than 80% of the new capacity comes from Asia, 20% from India and the United States. The Middle East has almost no new production capacity, and the European region is affected by rising energy prices and raw material shortages, oil and gas and chemical industries have been hit hard, Covestro, BASF and other large European petrochemical companies have a large number of production cuts and production news.

The recovery of ethylene consumption is weak under the pressure of stagflation

In 2023, the impact of geopolitics and the epidemic on the global petrochemical market gradually faded, replaced by continued high inflation and potential financial crisis risks in the United States and European countries. In fact, since the second half of 2022, the weak demand caused by inflation in the United States has been shown, even in the packaging field with a large consumption base and strong growth inertia, the consumption growth rate has fallen sharply from 6% in 2021 to 2%. In the second half of 2023, with the end of the destocking cycle, consumption weakness has recovered somewhat, but has not yet returned to pre-pandemic levels.

By region, the ethylene consumption performance of the world's regions is clearly differentiated, under the downward pressure of the economy, the demand in Asia has taken the lead in recovering, and the growth rate of ethylene consumption has picked up significantly, while the CIS countries, the Middle East and Western Europe have been affected by the energy crisis and geopolitical friction, and ethylene consumption has continued to decline. Among them, the risk of inflation and financial crisis in North America has intensified, and demand in downstream markets is weak, but the gap in Europe has made up for some North American consumption, and ethylene consumption has maintained its growth trend. In Northeast Asia, as the impact of the epidemic subsided, market demand gradually picked up; In the Middle East, the project production process has stalled for several years, and the Palestinian-Israeli conflict further dragged down demand in the second half of the year, and ethylene consumption showed negative growth; The shortage of energy supply in the European region still exists, especially as European enterprises import in advance and the end of the trade exemption period, Europe will seek alternative resources from the international market more, and the continuous negative growth of ethylene is difficult to reverse.

The operating rate of domestic ethylene plants is less than 85%

In 2023, China's new ethylene production capacity of about 6 million tons/year, the market supply pressure hit a record high. However, the market is still in the post-epidemic recovery stage, the terminal demand is weak, and ethylene consumption is less than expected. Even if oil and gas prices fall to benefit the industrial chain, the mismatch between domestic supply and demand has suppressed the overall profitability. Throughout the year, the industrial chain still maintained a loss, but the range was narrower than in 2022.

In 2023, China's total ethylene production capacity will exceed 50 million tons/year. Guangdong Petrochemical 1.2 million tons/year, Hainan refining and chemical 1 million tons/year refining and chemical integration device was put into operation in February, Zhejiang Xingxing New Energy 1 million tons/year light hydrocarbon cracking device was completed and put into operation in May, Jinghai Chemical 448,000 tons/year naphtha cracking device was put into operation in the second quarter, and the overall supply pressure increased sharply. In the second half of the year, there were fewer new ethylene projects, and only Baofeng Energy's Phase III coal chemical project was put into operation.

From the perspective of raw material structure, naphtha cracking is still the most important ethylene production route, and the capacity share has increased to 70%. The second is the MTO/CTO route, which is subject to carbon emission reduction and environmental protection policies in recent years, and the capacity share has declined to 14% year by year; Ethane /LPG (liquefied petroleum gas) light hydrocarbon route, with the satellite petrochemical, Zhejiang Xingxing New Energy and other projects put into operation, the capacity share rose to 8%.

It is worth noting that although oil prices have fallen compared with 2022, they are still at a high level, and the recovery of downstream demand is difficult to offset cost pressures. Constrained by oil prices and demand, the profitability of most petrochemical products is difficult to improve in the short term, and the downstream operating rate is difficult to increase greatly. The operating rate of ethylene plant in 2023 is less than 85%.

Ethylene demand growth momentum is insufficient

Due to the recovery of industrial production less than expected, consumer confidence is insufficient, the recovery of the terminal field is slow, the demand for downstream polyethylene, ethylene glycol and other products is sluggish, and domestic ethylene consumption is weak.

Specifically, at the beginning of 2023, China's purchasing managers index (PMI) quickly rebounded from the bottom to break through 50%, and the market is generally expected to usher in a rebound in the petrochemical products market, and speculative hoarding and speculation once pushed up the price of domestic bulk products. However, after the Spring Festival, the terminal market continued to slump, and the acceleration of real estate investment and exports dragged down, and the demand for polyethylene in the second quarter of 2023 was weak, even weaker than the level of the first quarter of 2022; The ethylene glycol market situation is more severe, the global economic downturn is difficult to change, the market consumer demand has weakened, the textile and apparel did not appear the expected consumption peak, and the domestic polyester port inventory is at a historic high. At the same time, many sets of ethylene glycol units such as Shenghong Petrochemical, Hainan Refining and Chemical, and Zhejiang Xingxing have been put into operation, and the new supply pressure has far exceeded that of 2022, and the domestic ethylene glycol units have deep losses, and the long-term mismatch pattern of supply and demand has further negatively affected ethylene consumption. In the second half of 2023, the main growth drivers of ethylene demand will still come from the growth of domestic policy demand areas and the improvement of domestic demand.

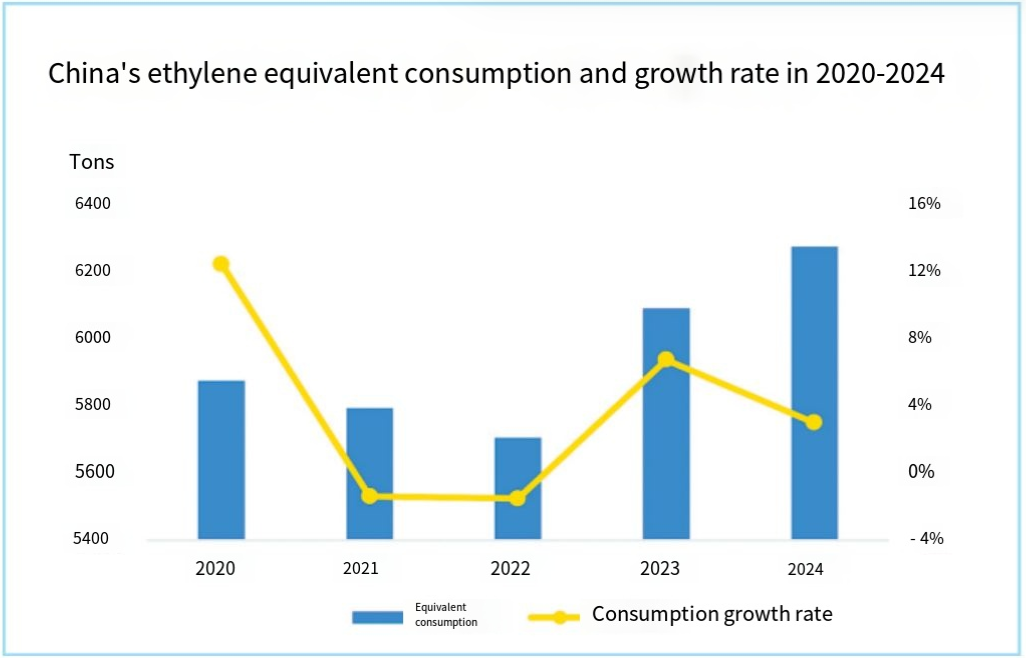

In the whole year of 2023, although the demand for ethylene is weak, taking into account the growth of upstream and downstream project construction and packaging, automobiles, agriculture and other industries, China's ethylene equivalent consumption growth rate of 6% to 7%, of which about 3% growth is caused by the low base in 2022, the actual increase is limited.

Ethylene routes continue to lose money

This round of global ethylene capacity expansion is basically coming to an end, and in 2024, the world will add 4 million tons of new capacity per year, all from China and the Middle East. The energy crisis and inflation risks may continue, but the global economy is expected to stabilize, downstream consumption continues to repair, and industry profitability is expected to improve.

Global ethylene entered the end of this round of capacity expansion peak

In 2024, the global ethylene production capacity is limited, only Iran's GachsaranPC (polycarbonate) 1 million tons/year ethane cracker and China's Yulong Petrochemical 2× 1.5 million tons/year naphtha cracker put into operation, a total of 4 million tons/year, ethylene production capacity will increase to 232 million tons/year.

As oil prices are still high in 2023, demand recovery is limited, and under the pressure of losses, the overall capacity of ethylene is released less than expected. In 2024, as the global economy recovers and demand picks up, device profitability is expected to improve.

The recovery trend of ethylene is obviously regionalized

Global economic and trade activities are under significant pressure in 2023, mainly due to the suppression of developed countries' interest rate hike policies on their own economies. Under the influence of high oil prices, increasing supply and weakening demand, the global chemical industry is in the trough of the business cycle. In 2024, with the end of policy tightening, the risk of stagflation will be significantly resolved, global trade activities will also bottom out, the demand for petrochemical products is expected to increase, and the chemical industry is expected to go out of the trough.

Market performance across the world's largest economies has diverged sharply. Among them, the inhibition effect of monetary policy tightening on the economy will continue to appear, it is expected that the economy will continue to decline in 2024, the risk of consumption inhibition caused by inflation and relatively loose monetary policy will inhibit the recovery of demand to a certain extent, but thanks to the low price of ethane, as well as the expansion of the demand gap in Asia and Europe, the demand for ethylene in the United States will still maintain positive growth. But growth will fall sharply. Although the European region has passed the winter of 2023 smoothly, from the production reduction of Russian natural gas and the implementation of a new round of trade ban on Russian naphtha in Europe, the impact of the energy crisis on Europe will continue, and high costs and high inflationary pressure will continue to suppress local consumption to a certain extent. Northeast Asia is boosted by economic recovery, slowing supply, improving exports and other factors, and overall demand is expected to recover.