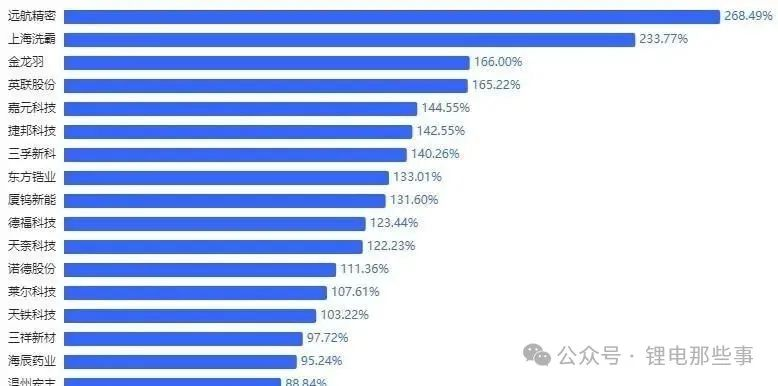

The "sky-high-priced blood" in solid-state batteries has finally been exposed! Recently, a cost list in the industry has sparked heated discussions. When you see that electrolytes account for 77.8% of the total cost of all-solid-state batteries, the lithium mine stocks in your hand suddenly don't seem so appealing anymore. It's like building a car where the cost of the engine is lower than that of the tires—can you believe it?

What exactly is this outrageously expensive electrolyte? Simply put, it is the core material that replaces the electrolyte in traditional liquid batteries. Currently, solid-state batteries follow two development routes: Semi-solid-state batteries mainly use oxide electrolytes, which is like "applying a patch" to the existing battery system; while all-solid-state batteries completely subvert the tradition, generally adopting sulfide electrolyte systems, which offer strong performance but come with a frighteningly high cost.

Take a look at the list of listed companies that are racing ahead in the electrolyte track: Shanghai Xiba has invested heavily in the pilot production line for sulfide electrolytes; Ganfeng Lithium has integrated oxide electrolytes into the battery packs of Dongfeng electric vehicles; the laboratories of Bettery and Enjie Co., Ltd. are piled high with samples of halide composite electrolytes. Even Xingyuan Material, which specializes in lithium battery separators, has begun adjusting its production lines to accommodate the coating process for oxide electrolytes.

But the most frenzied players are the raw material manufacturers. Sanxiang New Materials' zirconia powder is being competed for by multiple battery factories; Oriental Zirconium's zirconium salt orders are already scheduled into the first quarter of next year. Tianji Co., Ltd.'s lithium sulfide production lines are running 24 hours a day, with 300 tons shipped out monthly just in the East China region alone. Longbai Group has even modified its titanium dioxide production lines to create electrolyte raw material production lines, while Haichen Pharmaceutical's chemical workshops have suddenly started producing battery-grade sulfide precursors.

The revolution in solid-state batteries is also unfolding at the anode. Traditional liquid batteries use graphite as the anode, while semi-solid-state batteries have upgraded to silicon-based materials. For example, 贝特瑞 (Bettery)’s silicon-carbon anodes have been used in NIO’s 150kWh battery packs, and 翔丰华 (Xiangfenghua)’s nano-silicon particles can store 30% more lithium ions. But what is truly groundbreaking is the metallic lithium anode — in the solid-state battery samples showcased by 赣锋锂业 (Ganfeng Lithium), ultra-thin metallic lithium sheets, as thin as a cicada’s wing, have replaced graphite, pushing the energy density to a ceiling of 400Wh/kg.

Unfortunately, these cutting-edge technologies are still trapped in laboratories. Tianqi Lithium disclosed that the cost of its metallic lithium anode exceeds 2,000 yuan per square meter, while the hourly output of Tiantie Technology's lithium strip rolling mill is less than one-tenth of that of ordinary graphite production lines. Yinglian Co., Ltd.'s trial-produced composite lithium metal anode has just passed the needle puncture test, with a yield rate barely reaching 65%.

In contrast, cathode materials have seen the least change. In the solid-state battery samples from CATL and BYD, the cathodes still use the familiar nickel-cobalt-manganese ternary materials. Rongbai Technology’s high-nickel cathodes, after minor adjustments on liquid battery production lines, are directly supplied to solid-state battery projects. Zhenhua New Materials’ single-crystal materials have demonstrated stronger structural stability in CATL’s semi-solid-state batteries. Huayou Cobalt even stated: "The existing precursor production lines can fully meet demand for the next five years."

However, sulfide electrolytes have triggered a current collector crisis. Experiments have proven that traditional copper foil, when immersed in sulfides, corrodes and perforates within 72 hours. Yongjin Co., Ltd.’s developed stainless steel current collectors have entered the pilot test phase, with an astonishingly thin thickness of 8 microns. Even more ingenious is the composite metal foil solution: Putailai’s developed "plastic + copper plating" sandwich structure has passed a 120-hour high-temperature immersion test, with production costs only 15% higher than those of copper foil.

In the factory of Jiangsu Tiannai Technology, carbon nanotube conductive agents are being produced at full capacity. The usage of conductive agents in semi-solid-state batteries has surged to three times that of traditional batteries, with the consumption for 1GWh soaring to 120 tons. The conductive slurry production line of Daoshi Technology has just completed intelligent transformation, with monthly production capacity exceeding 2,000 tons. The purity of carbon nanotubes from Heimao Co., Ltd. has been upgraded to 99.9%, directly entering CATL's supply chain.

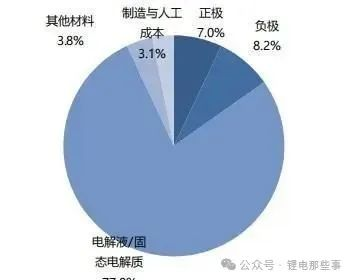

The figures in the cost ledger are still shocking. The current material cost composition of all-solid-state batteries clearly shows: 77.8% is spent on electrolytes, 8.2% on anodes, and only 7% on cathodes. Bettery's financial report shows that the gross profit margin of its silicon-based anodes reaches 42%, far exceeding that of traditional graphite products. Tianci Materials has invested a cumulative 980 million yuan in its solid-state electrolyte project over three years, and the first batch of orders will not be put into production to reduce costs until 2026.

The pilot production lines in laboratories are burning money every day. An engineering department supervisor at a leading enterprise revealed: "The waste loss of sulfide electrolyte powder alone accounts for 35% of the raw materials." For the third-generation solid-state battery cells trial-produced by Ganfeng Lithium, the electrolyte cost alone accounts for 62% of the entire battery. The quotation for zirconia raw materials from Sanxiang New Materials has increased three times in three months, with a cumulative increase of 18%.