The chemical fertilizer industry is a special branch of China's chemical industry and an important support for the development of China's agriculture. Over the past few decades, the chemical fertilizer industry has mainly focused on basic supply guarantee. However, with the structural adjustment of agriculture and the trend of refined development of chemical fertilizer enterprises, many development opportunities have been brought to chemical enterprises. In order to conform to the development direction in the next five years and improve the economic value of chemical fertilizer enterprises, chemical fertilizer enterprises attach great importance to the "15th Five-Year Plan".

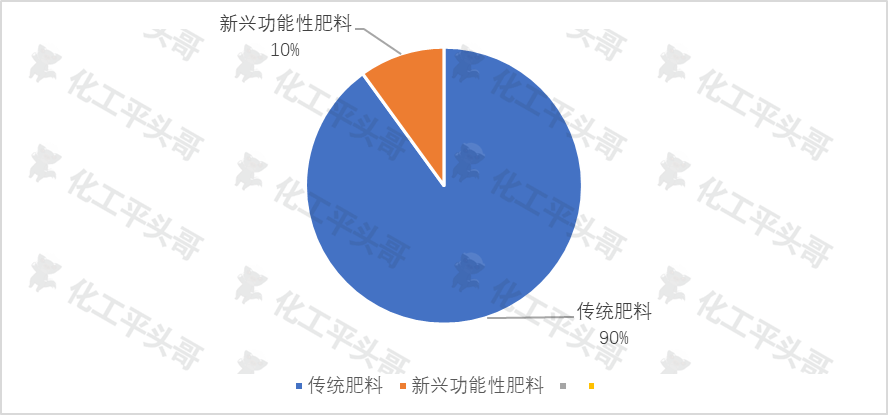

What is the current development status of China's chemical fertilizer industry?According to the statistical data from China's Ministry of Agriculture, in 2024, China's chemical fertilizer output reached 81.373 million tons, with a market scale of approximately 733.59 billion yuan, a year-on-year increase of 2.8%. It is expected to exceed 80 million tons in 2025. Among chemical fertilizer varieties, traditional fertilizers account for more than 90%, while organic fertilizers, biomass fertilizers, and functional fertilizers have a relatively low proportion but show a rapid growth rate in consumption.

In terms of capacity utilization, the overcapacity of traditional chemical fertilizers is obvious. The capacity utilization rate of the nitrogen fertilizer industry is less than 70%, while the production capacity of new-type fertilizers is releasing rapidly. Representative enterprises such as Stanley and New Yangfeng have a capacity utilization rate of over 90%. From this data, it can be seen that new-type fertilizers are quickly seizing the market of traditional fertilizers.

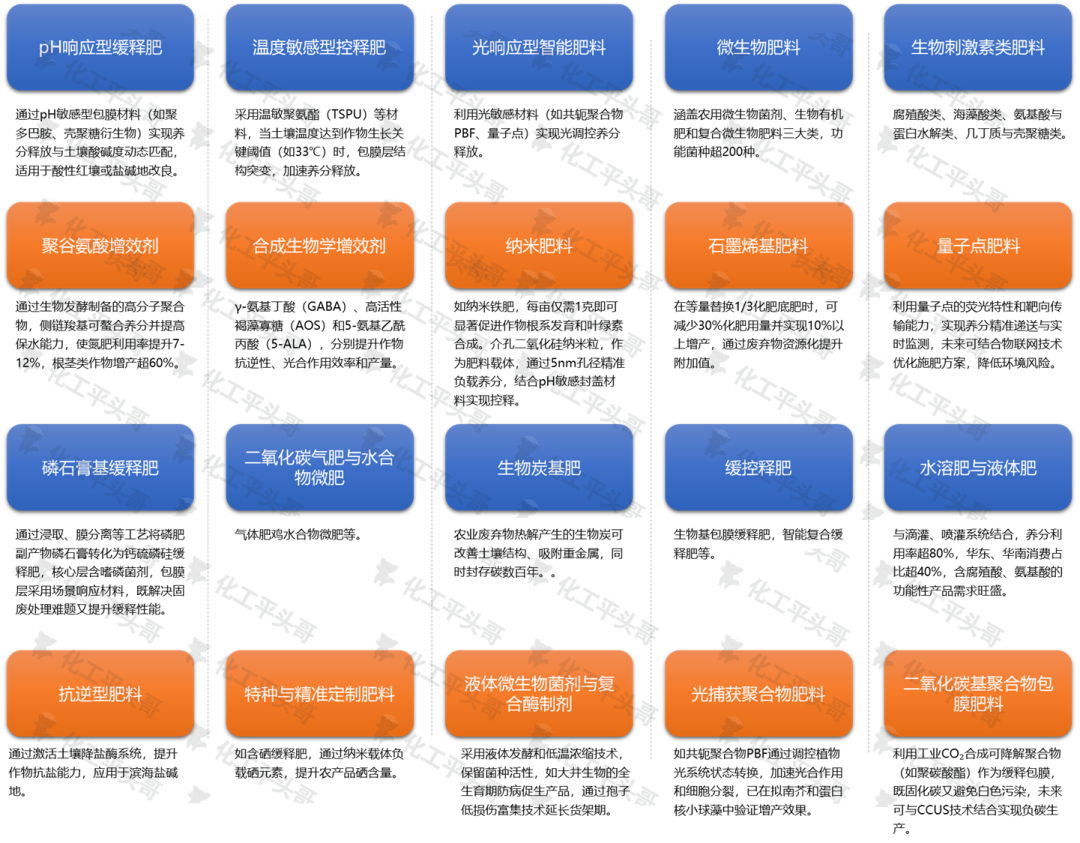

we believes that the next five years will be a critical stage for China's chemical fertilizer industry to transform from scale expansion to high-quality development. Basic supply guarantee has become a thing of the past, and high-quality development will be the mainstream in the future. The chemical fertilizer industry will gradually shift from single nutrient supply to crop full-life-cycle solutions, driven by both intelligent development and low-carbon initiatives, and extend the entire value chain from manufacturing to services. The scale of new-type fertilizers such as slow and controlled-release fertilizers, biomass fertilizers, water-soluble fertilizers, and liquid fertilizers will expand rapidly. Forward-looking fertilizers such as stress-resistant fertilizers, selenium-containing slow-release fertilizers, nano-urea, and phosphorus-solubilizing bacteria compound fertilizers will also be quickly popularized, and high-value-added fertilizers will gradually enter people's daily use. In addition, enterprises like New Yangfeng and Stanley have introduced AI to screen bacterial strains and used the Internet of Things to monitor the fermentation process in the production of biomass fertilizers. The high-end services and applications in the chemical fertilizer industry will also be an important development trend in the future.

In the next five years, chemical fertilizer enterprises should align with national plans and strategically anchor policy orientations.

In the next five years, chemical fertilizer enterprises should align with national plans and strategically anchor policy orientations.

The chemical fertilizer industry is a typical policy-oriented industry, and policies play a significant role in the development of this industry. Therefore, when formulating development plans for the next five years, chemical fertilizer enterprises should first align with national development plans and national-level strategies, and anchor themselves to policy orientations.

Chemical fertilizer enterprises should deeply integrate into policy systems such as the 14th Five-Year Plan for the Development of Raw Material Industry and the 14th Five-Year Plan for National Agricultural Green Development. They should focus on responding to the overall goals of increasing the fertilizer utilization rate to 45%, breaking through 65% in the comprehensive utilization rate of phosphogypsum, and raising the proportion of new-type fertilizers to more than 35%, so as to help achieve national goals from the perspective of enterprises. In addition, chemical fertilizer enterprises should rely on regional strategies such as the Yangtze River Economic Belt and the ecological protection of the Yellow River Basin to optimize the distribution of production capacity. They should develop relevant chemical fertilizer concentration areas based on local resources, such as phosphate compound fertilizer concentration areas relying on phosphate rock resources, Qinghai Salt Lake potash development concentration areas relying on potash resource aggregation, and "wind-solar-hydrogen-ammonia integration" concentration areas relying on synthetic ammonia by-produced by nitrogen fertilizer enterprises.

In the face of the national strategic layout, chemical fertilizer enterprises also need to formulate corporate carbon emission reduction roadmaps, clarify the timetables for the application of technologies such as CCUS (Carbon Capture, Utilization and Storage) and green ammonia, replicate the carbon emission reduction plans and technologies of successful enterprises, and make important strategic adjustments in the next five years to reduce carbon emissions and improve greenization in chemical fertilizer enterprises.

Over the next five years, chemical fertilizer enterprises should attach importance to industrial breakthroughs and technological innovation.

Industrial breakthroughs and technological innovations in chemical fertilizer enterprises are expected to become important development directions for chemical fertilizer enterprises in the future. If the right direction is chosen, the output value of chemical fertilizer enterprises will be greatly promoted in the next five years.

Regarding industrial breakthroughs and technological innovations, we believe that the following aspects need to be focused on.

First, technological breakthroughs in green and low-carbon synthesis, such as the technology of photovoltaic electrolysis of water to produce hydrogen coupled with ammonia synthesis. At present, enterprises like Yuntianhua and Xinlianxin have already laid out plans in this field.

Second, high-value utilization technologies of phosphogypsum, such as applications in high-strength gypsum, phosphogypsum plant cultivation substrates, phosphogypsum-based gels, and phosphogypsum ecological restoration. At present, enterprises including Chuanheng Chemical and New Yangfeng have successively implemented these technologies. It is expected that the comprehensive utilization rate of phosphogypsum in China will exceed 80% by 2030.

Third, fluorine and silicon resource recovery technologies. Recovering hydrogen fluoride from associated resources of phosphate rock and extending the downstream industrial chain based on hydrogen fluoride as a raw material is an important strategic positioning to get rid of dependence on fluorite, which is of great significance to phosphate compound fertilizer enterprises.

Fourth, technological breakthroughs in new-type fertilizers, such as the research and development of pH-sensitive and temperature-sensitive coating materials (e.g., nano-magnesium oxide, nano-calcium oxide) to achieve dynamic matching between nutrient release and crop demand, as well as bio-based slow-release materials. The introduction of gene-edited engineering strains can improve the efficiency of nitrogen fixation and phosphorus solubilization.

Fifth, actively building digital factories and engaging in the integration of IoT sensors and AI quality control systems. This can not only reduce energy consumption in chemical fertilizer production but also develop precise formulas by combining soil big data and crop models.

Over the next five years, chemical fertilizer enterprises should actively expand into the global consumer market, with a focus on advancing the layout of the Southeast Asian market.

Over the next five years, chemical fertilizer enterprises should actively expand into the global consumer market, with a focus on advancing the layout of the Southeast Asian market.

We believe that the trend of oversupply in China's chemical industry is obvious, and expanding into new consumer markets in the future will be one of the important directions for chemical fertilizer enterprises.

In terms of China's domestic consumer market, the eastern coastal areas mainly demand high-end water-soluble fertilizers and slow-release fertilizers to meet the needs of facility agriculture and high-value-added cash crops. In the central and western regions, functional fertilizers such as humic acid fertilizers and polyglutamic acid fertilizers are mainly needed to help improve saline-alkali land and save agricultural water. In the northeast and north China regions, the application of bio-organic fertilizers and microbial agents should be expanded to serve the protection of black soil and the reduction of fertilizer use and efficiency improvement in major grain-producing areas.

For the international chemical fertilizer consumer market, it is suggested that chemical fertilizer enterprises take stakes in or acquire overseas potash mines in the next five years, and establish long-term supply agreements with phosphate rock resource countries such as Morocco and Jordan. In Southeast Asian countries like Vietnam and Indonesia, as well as in African countries such as Nigeria and Tanzania, compound fertilizer production bases can be built to reduce costs by utilizing local natural gas and phosphate rock resources and avoid trade barriers. At present, some Chinese chemical fertilizer enterprises have been actively laying out the global market.

In addition, chemical fertilizer enterprises also need to actively export technologies globally, such as China's slow-release fertilizer technical standards, and radiate the European and African markets through the "technology authorization + localized production" model, so as to increase the proportion of chemical fertilizer exports in the next five years.

Over the next five years, chemical fertilizer enterprises should strengthen risk control and enhance the concept of sustainable development.

In the future, competition in China's chemical fertilizer industry will become increasingly fierce. Traditional fertilizers account for a large proportion, and large-scale enterprises will inevitably continue to seize market share, thereby bringing more market competition risks. Chemical fertilizer enterprises will achieve the goals of increasing industry concentration and market share through mergers and reorganizations, where large-scale enterprises will acquire small and medium-sized ones. This will eliminate small-scale and inefficient production capacity and realize sustainable development.

In addition, chemical enterprises will need to strengthen research on beneficiation technologies for medium and low-grade ores in the future, promote capacity optimization under the "slag-based production" policy, popularize zero-emission technologies, adopt advanced denitrification, desulfurization, and VOCs recovery technologies, and build a "coal-electricity-fertilizer-chemical" co-production system to achieve the sustainable development of chemical fertilizer enterprises.

We believe that the "15th Five-Year Plan" period will be a crucial five years for the high-quality development of China's chemical fertilizer enterprises and also a key period for completing the low-carbon transformation of traditional production capacity. On the basis of clarifying the current industrial status, chemical fertilizer enterprises can build a development framework featuring strategic focus, technological leadership, market diversification, and controllable risks, thereby achieving a leap from "scale expansion" to "quality improvement". This will provide core support for ensuring national food security and promoting the sustainable development of global agriculture.

In the next five years, chemical fertilizer enterprises should align with national plans and strategically anchor policy orientations.

In the next five years, chemical fertilizer enterprises should align with national plans and strategically anchor policy orientations.