Variable one: The global macro economy and China's economy are expected to weaken

Take Fitch's forecast: In September, Fitch raised its 2023 global growth forecast by 0.1 percentage points to 2.5 percent, reflecting the surprising resilience of the U.S., Japan, and emerging markets (EM) excluding China so far this year. Fitch upgraded growth in the U.S. by 0.8 percentage points to 2.0 percent, in Japan by 0.7 percentage points to 2.0 percent, and in emerging markets excluding China by 0.5 percentage points to 3.0 percent. Growth in emerging markets outside China was revised up 0.5 percentage points to 3.4 per cent. This more than offset a 0.8 percentage point downgrade to 4.8 per cent in China and a 0.2 percentage point downgrade to 0.6 per cent in the eurozone.

The growth differential between emerging markets, excluding China, and advanced economies is expected to widen. The growth gap between emerging markets outside China and advanced economies is expected to be close to historic levels this year, partly reflecting the early arrival of the monetary policy tightening cycle in emerging markets.

However, Fitch cut its global growth forecast for 2024 by 0.2 percentage points to 1.9 per cent, a sharp cut. Growth forecasts for the United States were cut by 0.2 percentage points to 0.3 percent, for the euro area by 0.3 percentage points to 1.1 percent, and for China and emerging markets (excluding China) by 0.2 percentage points to 4 percent. China and emerging markets excluding China were revised down 0.2 percentage points to 4.6% and 3.0%, respectively.

A hoped-for stabilisation in China's property market has failed to materialise, with new home sales likely to fall by a fifth this year. Housing, which accounts for a third of investment and 12% of China's GDP, has a strong multiplier effect on the wider economy. So far, easing has been ineffective, and export demand is falling.

Oxford Economics and others also gave a similar forecast, the overall macro economy will not necessarily recover as expected, perhaps more stimulus policies.

Variable two: The chemical industry landscape faces reshaping due to China's increased capacity

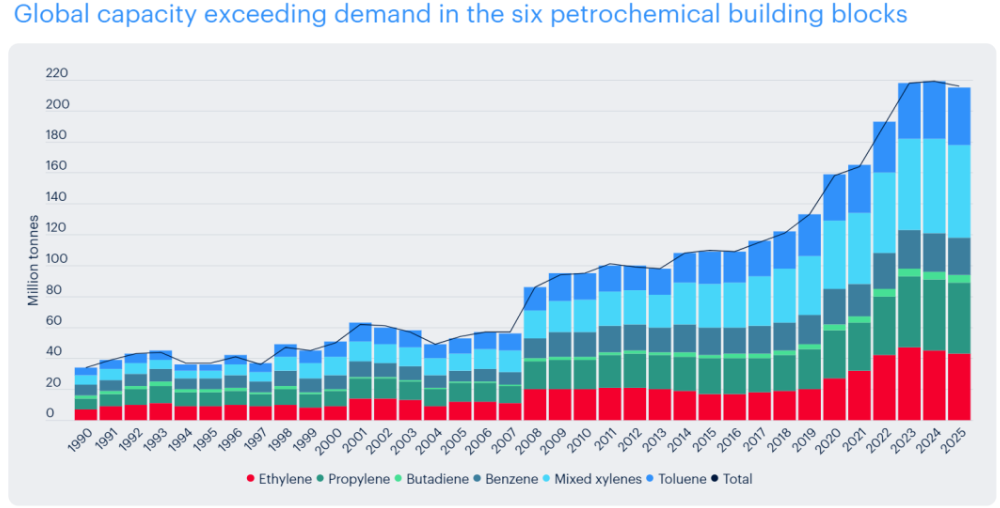

After several years of heavy capacity investment in China, as global capacity increases and demand weakens, the global petrochemical oversupply is expected to reach a record 218 million tons by the end of 2023, while China is continuing to add capacity, with nearly 140 million tons expected to come on stream by 2023. Far more than in previous years.

Against the backdrop of a deteriorating macroeconomic outlook and a strong US dollar, chemical market participants are having to face unprecedented uncertainty within the industry.

Short - and medium-term factors such as

Record industry overcapacity and weak profits across the industry

High raw material and energy costs will affect the short-term competitiveness and long-term viability of producers such as European producers

Competition from low-cost producers in the US and the Middle East has intensified

China became a net exporter of certain key chemicals and gained a foothold in the higher-volume specialty chemicals sector

Factors of long-term structural change such as

The industrial structure will gradually shift towards recycled materials and low-carbon intensive products

The pace of carbon-cutting legislation affecting trade patterns is accelerating

Key industries such as autos are changing dramatically, with electric vehicles replacing petrol and diesel cars

Adopt new technologies to replace traditional energy sources and materials

The transition to a low-growth economy in China and other demand-rich countries

Chemical companies must adapt, build flexibility into their operating models to maximise short-term opportunities and transform to succeed in a vastly different trading environment.

Given its importance in manufacturing, the chemical industry was one of the first to react when high inflation, rising interest rates and record energy prices began to dampen consumer spending in 2022. Chemical producers responded by cutting inventories and reducing costs to improve efficiency. Since then, global chemical production has continued to decline following the impact of the pandemic in 2020/21, falling by 5.3% year-on-year in the first quarter of 2023.

At the same time, China's longer-term structural growth slowdown begins in 2021. China's economy may be affected by unique factors outside of macroeconomic trends, such as real estate, that affect its economic growth. Some of the weakness is due to COVID-19-related shutdowns, but China has also shifted to redistributing wealth away from lending to key sectors such as housing.

The Chinese market accounts for about 45% of global demand for chemicals and petrochemicals. In 2022, China's polyethylene consumption is almost equal to that of the rest of the developing world combined, even though China's population is less than 30% of that of the rest of the developing world: 1.45 billion versus 5.2 billion. After the end of the largest ever government stimulus package, demand began to shrink as export markets weakened, the population aged and households shrank. This is despite the widespread expectation of even negative growth for most chemicals in China in 2021 and 2022, when consumption growth was widely expected to be in the single digits, which also contributed to the current oversupply.

China's excess chemical capacity has been increasing since 2014, five years after the government launched a plan to increase self-sufficiency in what is seen as a high-value sector. China currently accounts for 45% of global chemical production capacity and is expected to reach 62% market share by 2035, while Chinese chemical companies will gradually focus on innovative, more environmentally friendly products and higher value specialty chemicals.

In 2022, global overcapacity for six chemicals: ethylene, propylene, butadiene, benzene, mixed xylene and toluene averaged 191 million tonnes (with a market size of 2.3 billion tonnes). This figure is expected to rise another 10-15% to 218 million tonnes by 2025.

China's dominance is rapidly increasing in certain key chemical sectors, such as:

In 2022, China surpassed the United States to become the world's largest producer of ethylene, a core component of more than 75 percent of petrochemical products. In 2023, China is expected to add nearly 140 million tons of chemical and fertilizer capacity, a record high (dwarfed by the 90 million tons a year record set in 2014). In the next two to three years, China's ethylene production will be enough to meet domestic demand, and there may be surplus production for export.

In the above six chemicals, China's production capacity increased significantly in 2019 and will account for an average of 38% of world supply by 2022, a figure that is still rising.

China is currently the world's largest exporter of polyethylene terephthalate (PET) resin, refined ethylene terephthalate (PTA), polyvinyl chloride (PVC) and polyester fibers.

China's polypropylene (PP) exports increased from about 500,000 tonnes in 2020 to 1.3 million tonnes in 2022, while net imports almost halved, from 6.1 million tonnes to 3.2 million tonnes.

Economies of scale have also made China a larger producer of some fine and specialty chemicals, such as plastic additives. This development will have a significant impact on supply chains and pricing in the future.

Variable five: Uncertainties, such as the Russia-Ukraine war, Saudi Arabia, China and the United States

Tensions between key energy exporters and energy demand countries are expected to continue. Overall global political and economic trends in 2023 are expected to continue in 2024.

High oil prices are in line with the economic interests of Saudi Arabia, Russia and other countries. The official financial balance price of Saudi Arabia's crude oil is 78 US dollars per barrel, and Russia's financial balance has increased from 45 US dollars per barrel to 115 US dollars per barrel after the Russia-Ukraine war. However, the current economic status of major buyers such as China is not able to support high oil prices. The inflationary pressure in the United States has prompted the United States to do whatever it takes to curb the further rise in oil prices. The US election will also be an uncertain variable, with the price of oil exceeding $80 only once during Trump's presidency.

These factors have a profound impact on the overall energy landscape.

It is estimated that the chemical and petrochemical industry emits 920 million tons of CO2 equivalent per year, making it the third largest industrial sub-sector for direct CO2 emissions. Therefore, the need to report on Category 3 emissions and reduce the carbon footprint is becoming more and more important. Automation, new technologies and artificial intelligence are reshaping production processes, facilitating the development of new biodegradable and recyclable materials, while enabling chemical producers to reduce emissions.

As the circular economy takes shape, the demand for less resource-intensive products and recyclable materials, supported by increasingly stringent regulations, and the shift towards lower consumption and reuse, are reshaping long-term trends.

As suppliers adapt to slower growth, further market consolidation, changing demand, increased competition from China and emerging exporters, and wider adoption of technology and automation, the next decade will be a critical period for the evolution of the chemical supply chain.

Preliminary conclusions:

Overcapacity and weak demand, combined with record energy prices, are creating a perfect storm that will hit the industry like never before. Weak downstream demand makes the price of downstream products unable to timely feedback and support the rise in raw material prices, which is expected to cause the gross profit level of the overall industry to continue to decline. The whole industry will return to the destocking cycle position. The decline in gross profit level will force the old, broken, and old capacity to stop, rest, and inspect, thus forming a supply-demand balance state of low production capacity, low inventory, and low gross profit level.

2023 is a breathing year, because the enterprise is not clear, the market direction is not clear, so there is room for breathing, if the domestic real estate trend becomes clearer in 2024, the economic trend is weakening, the demand is insufficient, and the enterprise "lying flat" development, the industry as a whole is expected to be in the active destocking stage of the kitchen cycle. The transition from recession to recovery is expected to take a longer period of time.

However, for domestic leading chemical enterprises, endangered organic, there is no excess capacity, only eliminated capacity. In 2024, it is expected that it will be the trough of a major cycle of the chemical industry, with low production capacity, low inventory and low gross profit. Are enterprises ready for winter? Will 2024 be the first year of a new shakeout in the chemical industry? How should we prepare?