On October 8, the commencement ceremony of 27/600,000 tons/year propylene oxide/styrene (including ethylbenzene) device (referred to as "POSM device") of Guangxi Petrochemical, refining and chemical integration transformation and upgrading project was held in Qinzhou Port. It is understood that the POSM device of Guangxi Petrochemical project is the first set of similar devices independently designed, purchased and constructed by petrochina. The device is an important part of Guangxi Petrochemical transformation and upgrading project, which improves the downstream products and enrichis the industrial chain, and also has representative significance for the overall implementation of the project. POSM plant scale 270,000 tons/year propylene oxide and 600,000 tons/year styrene, a total area of 151,435 square meters, including ethylbenzene, peroxide, epoxidation, PO refining, benzene ethanol dehydration, styrene refining, hydrogenation, environmental protection, public works and auxiliary facilities, furnace area, device tank area, on-site cabinet room, device substation and other units.

POSM device products market space is broad

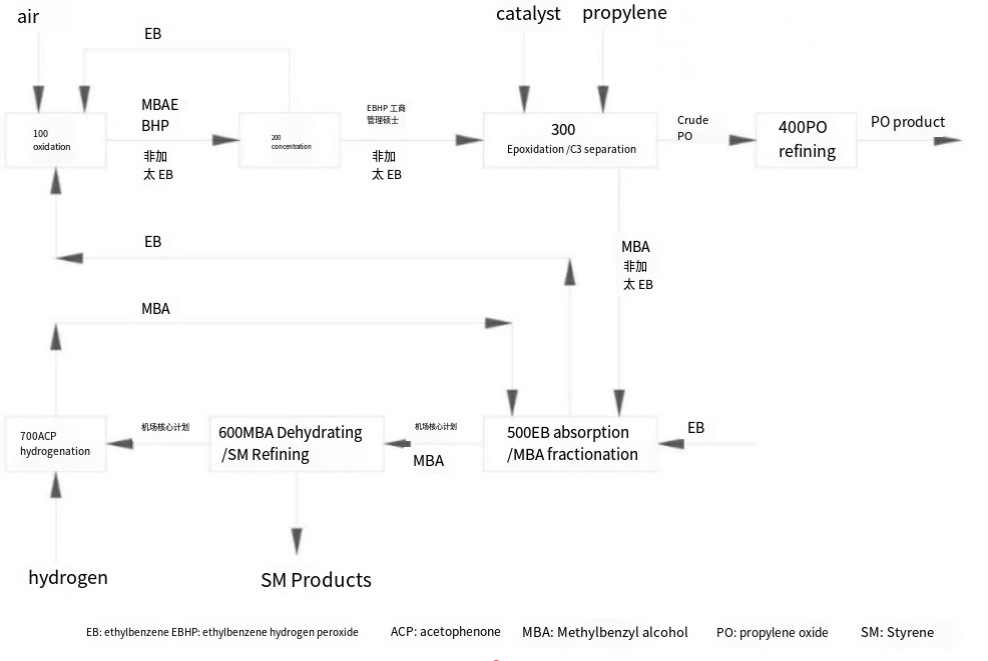

The upstream raw materials of POSM plant are mainly ethylene, propylene and benzene produced by refining and chemical integration project, and then propylene oxide and styrene monomer are produced by co-oxidation method.

As the second largest production process of styrene in China, the co-product of POSM process is propylene oxide. Propylene oxide is an important intermediate in petrochemical industry, is the second largest downstream of propylene, its upstream involves a variety of production processes, the downstream is the most widely used in the production of polyether polyols, the terminal involves furniture, automobiles, refrigerators and other industries.

Propylene oxide production capacity or up to 10 million tons

In the past five years, the utilization rate of China's propylene oxide production capacity has been more than 80%, and the production capacity has begun to accelerate after 2020, which is also accompanied by the decline of import dependence. Subsequently, with the release of new production capacity in China, propylene oxide will complete import substitution and seek export.

According to Refinitiv and Bloomberg data, as of the end of 2022, the global propylene oxide production capacity of about 12.5 million tons, mainly concentrated in Northeast Asia, North America and Europe, of which China's production capacity of 4.84 million tons, accounting for nearly 40% of the world's first. It is expected that from 2023 to 2025, the world's new propylene oxide production capacity will be concentrated in China, with an average annual capacity growth rate of more than 25%, and by the end of 2025, China's total production capacity will be nearly 10 million tons, and the global capacity will account for more than 40%.

In terms of demand, China's propylene oxide downstream is dominated by polyether polyols, accounting for more than 70%, and polyether polyols have been in a situation of excess capacity in recent years, and more production needs to be alleviated by export. According to the end demand area, we found that the production of new energy vehicles, furniture retail sales, exports and the accumulation of propylene oxide apparent demand have a high correlation year-on-year. In August, furniture retail sales and the cumulative production of new energy vehicles performed better, furniture exports continued to fall year-on-year, and the better performance of furniture domestic demand and new energy vehicles will still promote the demand for propylene oxide in the near future.

Is the era of styrene surplus coming?

As POSM co-produced styrene, its own capacity is also in the expansion cycle. In recent years, China's styrene production capacity and output have grown rapidly, and the total domestic styrene production capacity in 2022 will be 17.37 million tons, an increase of 3.09 million tons over the previous year. This year, the domestic styrene production capacity continues to usher in a large outbreak, if the planned equipment are put into production on schedule, the total production capacity will reach 21.67 million tons, an increase of 4.3 million tons.

In 2023, the new production capacity is basically completed, and the annual production capacity growth rate is 20%, and it is expected that more than 2 million tons will be put into production in 2024, and the production capacity growth rate is about 10%. At present, the styrene external raw material plant is sometimes in a state of loss, and the average annual operating rate has dropped to less than 75%. In the future, the loss of styrene and propylene oxide, and the profit situation of POSM devices will change, which will help accelerate the capacity clearance of the styrene industry.

In the past two years, the production profits of styrene enterprises have continued to be compressed, and the loss of the industry has become a normal phenomenon. In 2022, except for the third quarter of the industry has a certain profit, the rest of the time is basically in a loss situation, and the loss is between 400 and 800 yuan/ton. In 2022, the average profit level of styrene is -379 yuan/ton, and in the first half of this year, the average profit level of styrene is 34.75 yuan/ton. It is expected that in the next few years, styrene will be in a long-term break-even or even a loss state.

2023 to 2025, the domestic styrene industry chain and a large number of new devices put into operation, is bound to have a huge impact on the supply and demand of styrene, the market will experience the process of rebalancing, is expected to show the following characteristics: first, the domestic styrene plant operating rate decline year by year, processing profits are compressed or even disappear; Second, in view of the shortage of pure benzene resources, the price of pure benzene may remain high, and the styrene non-integrated plant has the possibility of long-term loss and shutdown; Third, the import volume has declined year by year, but because the US dollar contract has the L/C90 (letter of credit 90 days after sight payment) payment advantage, and the internal and external arbitrage window will be opened in stages, the styrene import source still has a place in the domestic market; Fourth, the export volume increased significantly, China's styrene exports increase is the trend of The Times, but the future export volume growth is far less than the growth of China's styrene production capacity, export trading partners from South Korea, India, Southeast Asia will expand to Turkey, Brazil, Belgium, South America and other ocean-going areas. For domestic production enterprises, increasing export qualifications and expanding overseas markets is also a way to survive in the market in the future.