On December 1, the fourth set of 260,000 tons/year acrylonitrile plant of Shenghong Sierbang Petrochemical was put into operation in Jiangsu Lianyungang Petrochemical Industry Base, producing high-grade acrylonitrile. At this point, Shenghong acrylonitrile production capacity rose to 1.04 million tons/year, which marks Lianyungang petrochemical industry base, becoming the world's largest acrylonitrile production base.

Acrylonitrile is an important raw material of the three major synthetic materials (plastics, synthetic rubber, synthetic fiber), its upstream raw materials are propylene, liquid ammonia, the downstream is mainly acrylonitrile-butadiene-styrene (ABS) resin, acrylic fiber, acrylamide, carbon fiber, etc., widely used in aerospace, wind power generation, automotive, machinery, electronics and other fields. However, this kind of basic material with multi-purpose and large quantity and wide area has needed a large number of imports in China. From 2011 to 2013, China's annual acrylonitrile imports exceeded 500,000 tons, and the import dependence exceeded 30%.

In 2013, Shenghong started construction of the first acrylonitrile plant with an annual output of 260,000 tons in Lianyungang Petrochemical Industry Base, which was successfully started in 2015.

Since 2016, China's acrylonitrile imports have been significantly reduced, and the import dependence has also been significantly reduced. In 2016 and 2017, China's acrylonitrile imports were 306,100 tons and 270,800 tons, respectively, and the import dependence was 13.7% and 12%, respectively. While promoting import substitution, Chinese acrylonitrile enterprises have also accelerated their participation in the global market and filled the gap in overseas markets.

Production capacity is concentrated in East and Northeast China

The industrial production methods of acrylonitrile mainly include propylene ammoxidation and propane ammoxidation. At present, more than 90% of the world's acrylonitrile plants are produced by propylene ammoxidation, the main raw materials are propylene and synthetic ammonia, and the by-products are hydrocyanic acid, acetonitrile and ammonium sulfate.

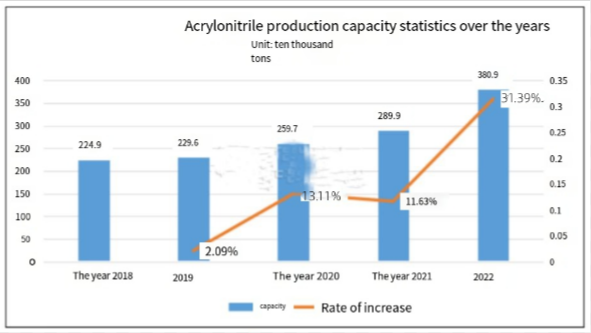

In 2022, the global acrylonitrile production capacity was 8.53 million tons/year, an increase of 11.9%, and the production capacity was mainly distributed in Southeast Asia (66.37%), North America (19.55%) and Europe (9.91%). In 2022, the world's new acrylonitrile production capacity totaled 910,000 tons/year, all concentrated in China, and China's production capacity accounted for 44.7% in 2022, making it the world's largest acrylonitrile production capacity region.

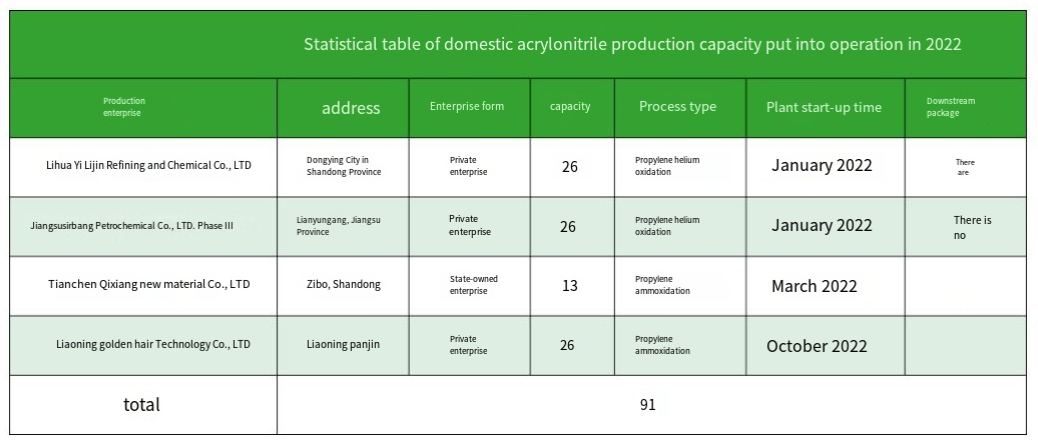

Before 2021, the domestic acrylonitrile production capacity increased steadily, and the expansion of 2022 production capacity accelerated, and the total production capacity of the industry increased to 3.809 million tons/year by the end of the year, with a capacity growth rate of 31.4%, accounting for 44.7% of the global total production capacity. Among them, the industry accounted for the top four enterprises (Sierbang Petrochemical, Shanghai Secco, Zhejiang Petrochemical, Jilin petrochemical) total production capacity of 2.272 million tons/year, accounting for 59.6% of the country's total production capacity. From the perspective of production technology, all of them are propylene ammoxidation process. From the perspective of regional distribution, East China and Northeast China are the main regions, with a total production capacity of 3.304 million tons/year, accounting for 86.7%.

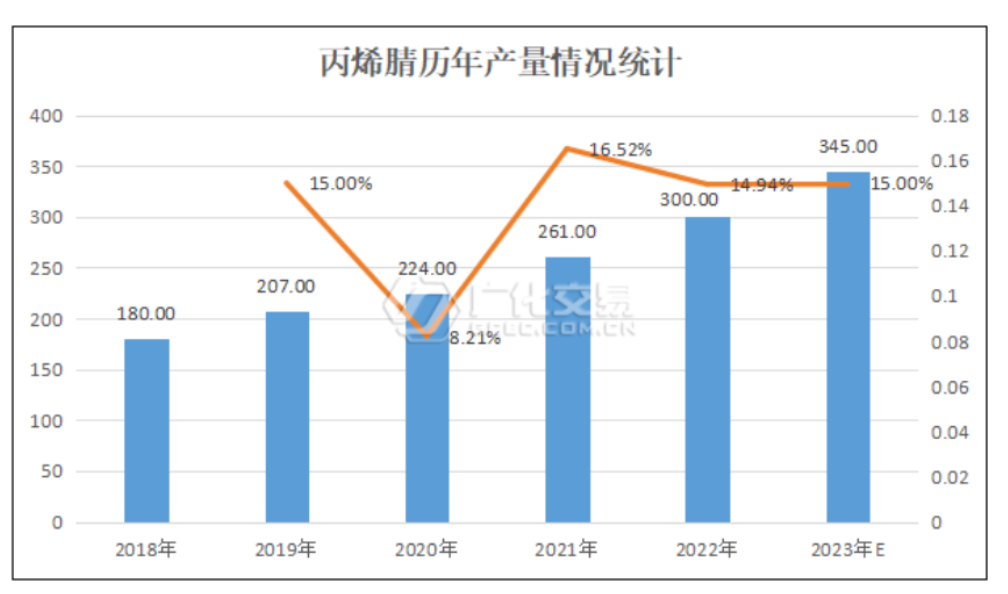

From the annual production point of view, the domestic acrylonitrile production shows a rising trend year by year, the output in 2022 is about 3 million tons, an increase of 14.94%, and the output is expected to reach 3.45 million tons in 2023, a year-on-year growth rate of 15.00%.

From the annual production point of view, the domestic acrylonitrile production shows a rising trend year by year, the output in 2022 is about 3 million tons, an increase of 14.94%, and the output is expected to reach 3.45 million tons in 2023, a year-on-year growth rate of 15.00%.

The glut is getting worse

The glut is getting worse

In the next five years, with the continuous release of refining and chemical projects, the domestic acrylonitrile production capacity will also increase significantly. According to the statistics of planned installations under construction, the total production capacity of acrylonitrile in China in 2023 will be 4.399,000 tons/year, and there will still be 3.26 million tons/year of new production capacity planned for 2024-2027, and the total domestic acrylonitrile production capacity is expected to reach 7.659 million tons/year by 2027. 2023-2027 China's average growth rate of acrylonitrile production capacity will reach 16.6%. The ABS industry, which is the main demand growth point in the downstream field, is also facing an oversupply situation, so the overall demand growth is far less than the supply growth. It is expected that the growth rate of acrylonitrile production capacity will slow down in 2023-2024, during which the excess resources will gradually be digested through the follow-up of downstream demand and the increase in exports, and the oversupply situation will be alleviated to a certain extent. Starting in 2025, a new cycle of capacity expansion will be entered, when the surplus situation will be more prominent.

ABS is still the main downstream demand growth point

China's acrylonitrile downstream consumption areas are more extensive, but mainly concentrated in the three major fields of ABS, acrylic fiber and acrylamide, in addition to nitrile latex, nitrile rubber, polymer polyol and carbon fiber industries. According to statistics, domestic ABS production in 2022 is 4.425 million tons, accounting for 41% of the total acrylonitrile consumption; The production of acrylamide in 2022 will reach 680,000 tons, and the consumption will account for 20%; Acrylic fiber consumption increased significantly compared with last year, the annual output of 560,000 tons, consumption accounted for 20%; In addition, the demand for nitrile latex industry is shrinking, and the industry output will plummet to about 550,000 tons in 2022, accounting for 5% of consumption; Carbon fiber industry growth accelerated, consumption accounted for 4%.

China's acrylonitrile downstream consumption area is more concentrated, mainly distributed in East China and Northeast China, the two regions accounted for 84% of the total domestic consumption. Among them, East China has gathered three major downstream ABS, acrylic fiber and acrylamide fields of major manufacturers, other small and medium-sized downstream enterprises are mainly distributed in East China, accounting for 62% of consumption; The northeast region also mainly concentrated three downstream factories, accounting for 22%; In North China, Tianjin Dagu ABS factory and Hebei acrylic fiber and nitrile latex factory, accounting for 7%; In central China, acrylamide factories are mainly concentrated in Henan, accounting for 4%; Some ABS and acrylamide factories are distributed in South China, accounting for 5%.

In the next five years, in the downstream fields of acrylonitrile in China, the ABS industry is still the main demand growth point. Thanks to the promotion of industry policies and new energy vehicles and other fields of demand, coupled with the stimulation of high profits of enterprises in the past few years, the ABS industry has also attracted more capital to enter, and between 2023 and 2025 for its new capacity investment cycle. According to statistics, as of 2026, the new capacity of domestic ABS resin will exceed 5 million tons/year, however, under the high capacity expansion cycle, the domestic ABS industry will also face an oversupply situation, so the capacity utilization rate will decline in the next five years. It is expected that the capacity utilization rate of the domestic ABS industry will drop from 80% to 70% in 2023-2027, and the output will increase from 6 million tons to 7.4 million tons, with a compound growth rate of 5.4%, which is weaker than the capacity growth rate of 5.8%.