In the modern business world, countless star enterprises and even industrial giants have gone bankrupt due to debt problems. For example, HNA and Evergrande, which were once powerful but later fell into bankruptcy reorganization, are all cautionary tales.

Looking at the 20-year development history of China's and even the global lithium battery industry, especially in the past decade, the industry has gone through several rounds of crazy unbridled growth and brutal reshuffling. According to statistics from Oriental Securities, for instance, in the five years from 2017 to 2023, after a major reshuffle in China's power battery industry, the number of battery manufacturers capable of matching vehicle models dropped from 81 in 2017 to 36 (as of April 2023), a decrease of 55.56%. By 2024, the number of battery enterprises participating in supporting facilities further reduced to 25.

During this period, most of the fallen star enterprises and even industrial giants "died from capital crises caused by cash flow 断裂".

Now, under the impact and influence of a new round of major retreat in the lithium battery industry, it may trigger another wave of industrial debt crises.

This is not an alarmist talk. Let's first look at a set of data compiled by 24 Tide Industry Research Institute (TTIR):

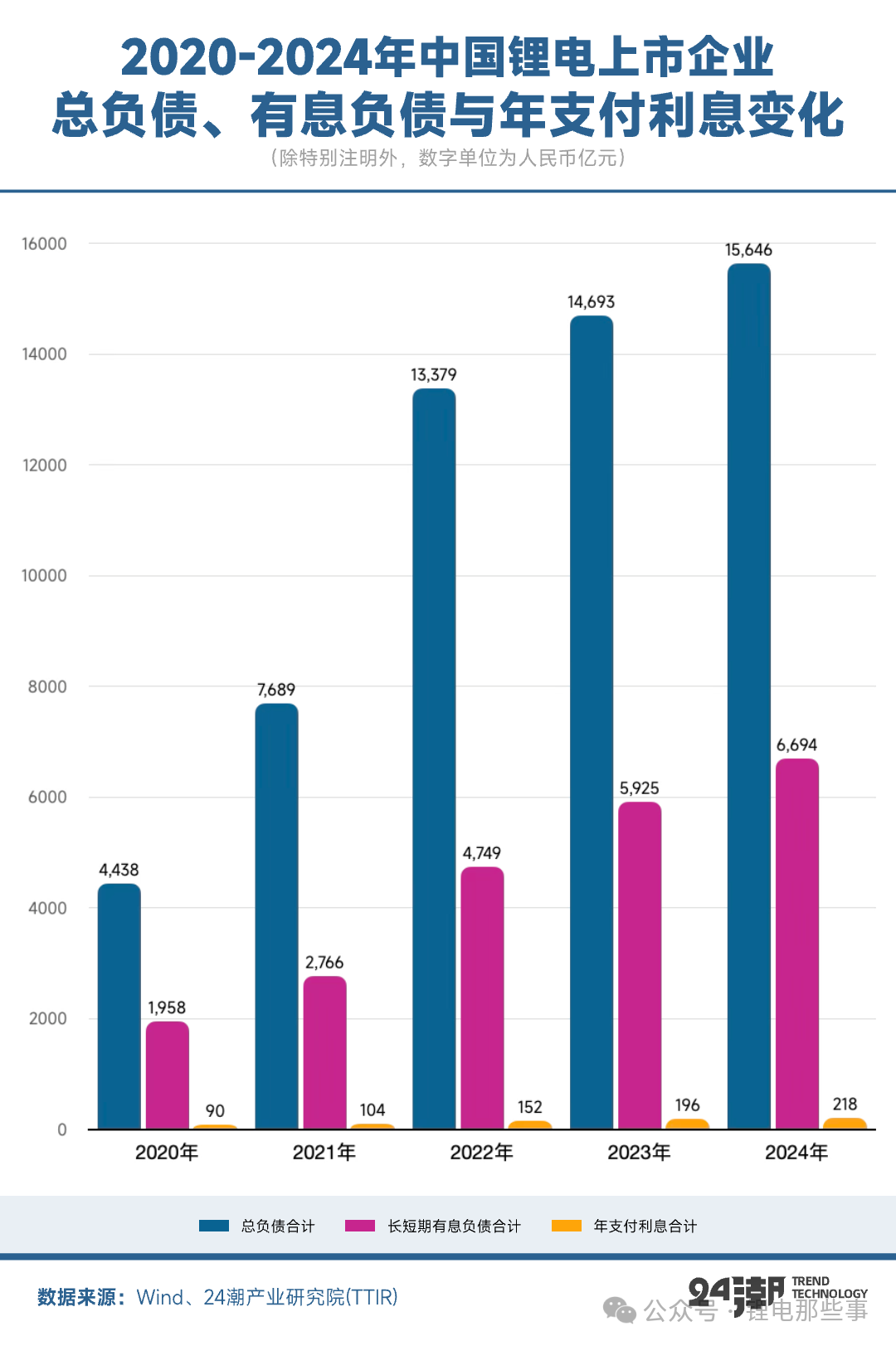

- Over the past five years (2022-2024), the total liability scale of China's listed lithium battery enterprises (including some IPO enterprises) has increased from 0.44 trillion yuan to 1.56 trillion yuan, a growth rate of 252.55%;

- In five years, the scale of long-term and short-term interest-bearing liabilities of China's listed lithium battery enterprises has risen from 195.8 billion yuan to 669.4 billion yuan, with an increase of 241.88%;

- During the same period, the interest expenses paid by China's listed lithium battery companies have grown from 9.024 billion yuan to 21.835 billion yuan, a growth rate of 141.97%.

When an industry is in a phase of sustained and rapid growth, massive debts and interest payments naturally do not pose a problem. However, when the industry as a whole stalls or even faces a crisis of sharp decline, these can become an unbearable burden for the sector. According to previous statistics from 24 Tide Industry Research Institute (TTIR), in 2024, the total operating revenue of over 100 listed lithium battery companies dropped by 11.87% year-on-year, with the growth rate falling by 11 percentage points compared to the same period in 2023. Their overall net profit attributable to shareholders plummeted by 67.27% year-on-year, marking the second consecutive year of a huge decline (the drop was 47.69% in 2023). The industry's blood-making capacity (net operating cash flow) also decreased by 18.38% year-on-year, with the growth rate declining by 61.01 percentage points from the same period last year. What's more, the net financing scale plunged by 81.91% year-on-year, and the net capital value also dropped by 20.32%, among other indicators.

In addition, as shown in the table below, the annual interest expenses of China's listed lithium battery enterprises have exceeded the increase in operating income and net profit for two consecutive years (the 2023 and 2024 fiscal years). In other words, the existing capital of the industry is continuously being overdrawn.

This is only data at the level of listed companies. The severe survival situation of many small and medium-sized enterprises is likely to exceed many people's imagination. Data from Qichacha shows that in 2024, the number of energy storage enterprises in China with abnormal registration statuses—such as deregistration, revocation, cancellation, liquidation, suspension of business, closure, delisting, and being ordered to close—has approached 30,000, among which more than 3,200 energy storage enterprises were established for only one year.

There is an industry consensus that "competition has entered a deep-water zone, and many companies are on the verge of life and death." We believe that under the current industrial situation, the importance of financial health cannot be overemphasized. Facing the industry's cold winter, companies with sound financial health will have sufficient ammunition to survive the cycle and become winners, while those with fragile finances will face severe tests. It is not ruled out that more enterprises may face debt defaults or even bankruptcy in the future.

Therefore, 24 Tide Industry Research Institute (TTIR) believes that at the current point in time, researching and analyzing the financial health index of China's listed lithium battery companies is of great significance to operators, creditors, investors, the government, and other parties.

In this article, 24 Tide Industry Research Institute (TTIR) has formulated the "Ranking of Financial Health Index of China's Listed Lithium Battery Enterprises (2024)" with reference to practices related to corporate credit ratings and bond credit ratings, and based on two major dimensions and 8 core indicators (in 2024):

- Capital structure, including asset-liability ratio and total debt capitalization ratio;

- Debt-servicing capacity, including quick ratio, operating cash flow to current liabilities ratio, cash-like assets/short-term debt, EBITDA interest coverage ratio, total debt/EBITDA, and total debt/net operating cash flow.

The ranking shows that 27 listed lithium battery enterprises are in a "leading" position in terms of financial health, 20 enterprises are under financial "pressure", and 15 enterprises are already in the "danger zone". It is believed that the ranking can provide some reference value for readers to gain a more intuitive and in-depth understanding of the financial health of enterprises. For the specific indicator weights and scores, please refer to the table below. Readers are also welcome to provide corrections and supplements.